We will aim the readership toward a new blog, since it seems very much like the same old wine… decanted into new bottles, here — at least as of last evening’s GAAP quarterly losses call. Enjoy — and be enlightened. These are very difficult business models to break even on, even at larger scales.

We will aim the readership toward a new blog, since it seems very much like the same old wine… decanted into new bottles, here — at least as of last evening’s GAAP quarterly losses call. Enjoy — and be enlightened. These are very difficult business models to break even on, even at larger scales.

And… the stock is now down around 3% — in after-hours NASDAQ trading, as a result.

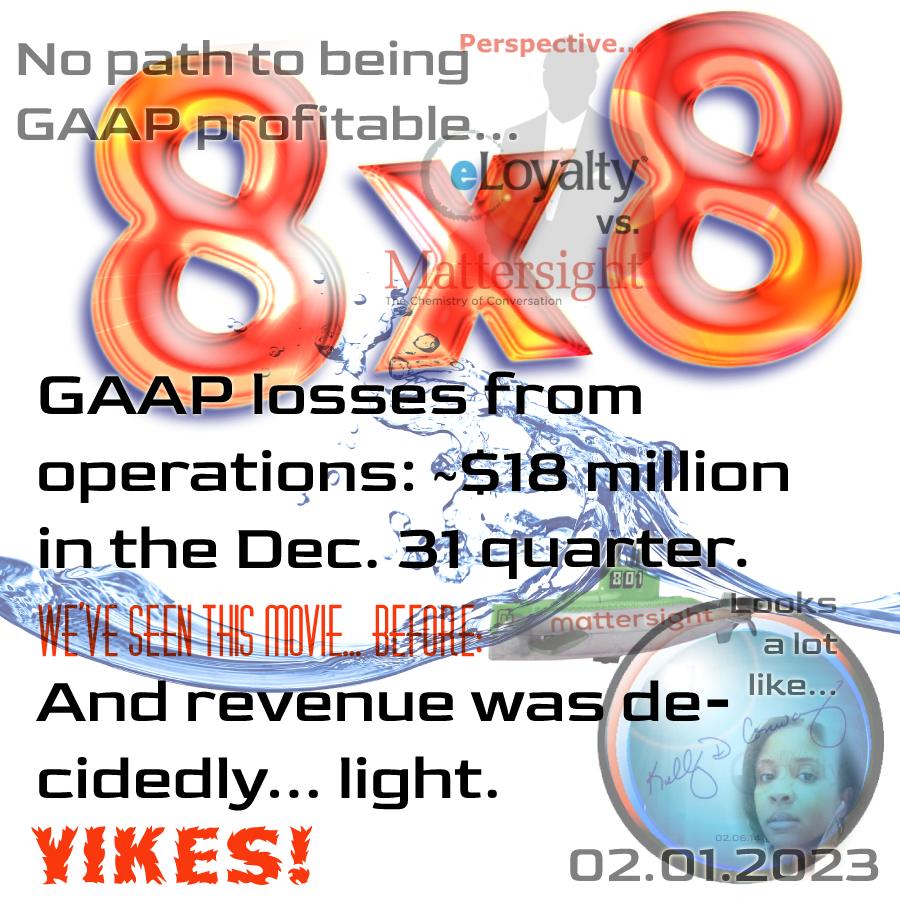

It is, in fact, inappropriate to call losses per share (GAAP)… earnings (Non-GAAP), whether per share, or not so — even on a fully-disclosed non-GAAP basis. This quarter, 8X8 ballooned its accumulated deficit by about $18 million… and chewed through another $63.7 million in losses from operations over the last nine months, which is consistent with GAAP loss from operations of ~$18 million — in just the December 31 quarter alone.

Sadly, 8X8 is tonight sounding more than just a little… like the old Mattersight — a company that was in the same vertical, before a “fire sale” acquisition by the larger Israel based NICE, Inc. We’ve seen… this movie, before.

For over 20 years, that company lost money — but touted its “customer wins”. It turned out that customer wins aren’t worth much, if the service / product is not priced (or worse, not valued in the marketplace) at a level that lets it at least cover all expenses — of being in these businesses.

That is the fundamental problem of these call center and voice solution businesses: there is no moat, and many large companies bidding for a set of clients that can afford to shop around for the lowest prices.

In sum, the model with clients is just not… sticky enough.

At this point — despite being much larger than Mattersight ever was — and getting close to being able to challenge NICE on foot-print overall… 8X8 simply cannot reliably be expected to be able to reduce expenses enough, or increase pricing enough… to ever make consistent net GAAP earnings per share.

Thus the “7% Solution” layoffs, just two weeks ago.

Thus the “7% Solution” layoffs, just two weeks ago.

In a future post, we will outline why this company’s debt load… is going to make the future here… very, very questionable, even for survival — for more than five years.

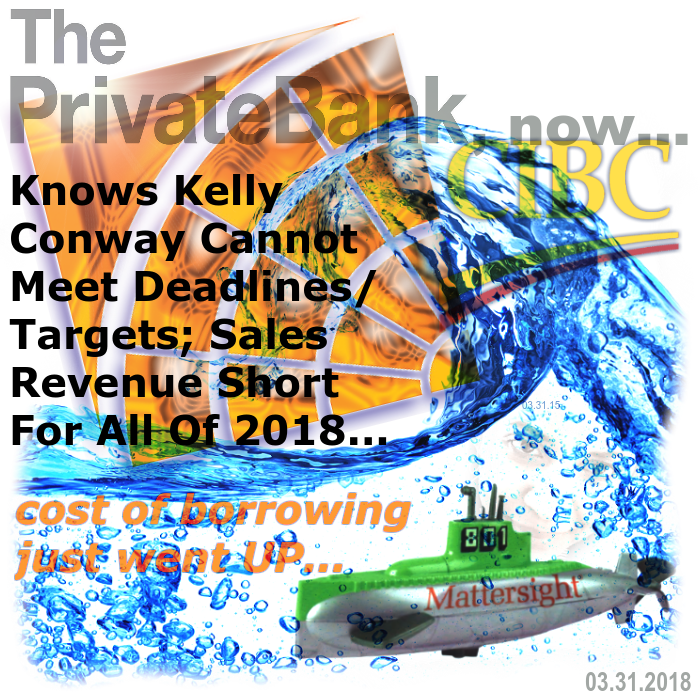

We saw it back at Mattersight — as well. And we saw that CEO, Kelly Conway, go on and on about “improving margins” on a non-GAAP basis, and still it was taken off the market at $2 a share — a fire sale (from $22/share just four years earlier) — because… it was (as 8X8 now is!) LOSING MONEY.

In sum — things are going to get significantly worse before they get better (if they ever do), on a GAAP basis. And in the end, stocks are only worth their future GAAP net cash flow, net of all expenses.

Damn. But… the more things change, the more they… stay the same.